We’ve all heard the advice that one of the best ways to get your finances under control is to start a budget – which is completely true. The problem is knowing just how to do it.

However, it can be hard to know not only how to do this, but how to actually stick to it.

So we’ve created the ultimate guide to the best budgeting methods out there to help you find one that will actually work for you.

TAKE BACK CONTROL OF YOUR FINANCES

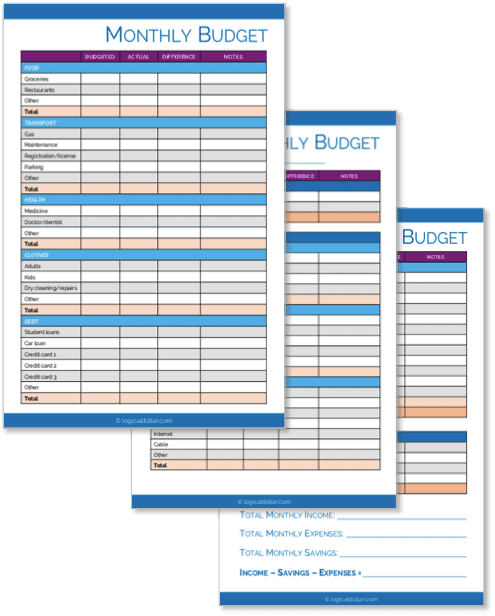

Our free budget planner will help you to quickly and easily take control of your money – instead of it controlling you.

Get it free for a limited time!

You’ll also join our mailing list to get updates on how to manage your money – unsubscribe at any time at the end of each email.

No more dreading going over numbers at the end of each month.

Or feeling guilty because it’s not even halfway through the month and you’ve already blown your spending targets.

Instead, check out this list to get some ideas on what may be the best system for you to manage your money each month.

And get ready for the feeling of knowing that your bills are paid, you’re chipping away at your debt and your savings are heading in the right direction.

Best budgeting methods

1. The 50/30/20 Budget

The 50/30/20 budget – sometimes also known as the balanced money technique or written as the 50.20/30 rule – is easily one of the most commonly used budgeting methods out there.

And the reason is simple: it works.

What is the 50/20/30 budget rule?

This rule involves spending 50% of your after-tax income on your needs, 20% on your “goals” and 30% on your “wants”.

This consists of the following:

- 50% needs: These are things that you absolutely have to pay, no matter what. This could include things like rent or your mortgage, grocery costs, insurance and utilities.

- 20% goals: This are the funds you’ll be allocating towards your financial goals. Looking to increase your savings, pay off debt (except your mortgage) or contribute towards your investments? This is where that money comes from.

- 30% wants: These are the things that make life just that little bit nicer – but that you could live without, if needed. For example, grocery costs come under “needs” but if you like to eat out from time to time, use the money in this pot.

What are the advantages of this?

This budgeting method is great for making sure you know exactly where all your money is going. It also lets you easily see if you’re over-spending in a specific category.

For example, if you get halfway through the month and realise you’re out of cash in your “wants” category, it’s time to take a good, hard look at your spending to see where you can cut back.

This method is also great for making sure that you’re working towards your goals every month and that all your payment obligations – or your “needs” – are taken care of before the fun stuff kicks in.

Finally, it’s a super simple way to stick to a budget. Gone are the days of having 12 different buckets which you have to shuffle your money between.

Instead, anyone can follow three categories and make sure their money is going exactly where it should.

Personal Capital

Our pick: Best budgeting app

Easily our choice for the best app to help you manage your money better.

Create a budget, track your spending automatically, receive personalized advice, get alerts about hidden fees and a ton more – and it’s all free.

What you should keep in mind

For some people, the simplicity of this budgeting method can also be its downfall.

Some people thrive in knowing they have a certain amount to spend on food and a certain amount to spend on utilities – rather than it all being pooled together under “needs”.

Another issue that comes up with the 50/20/30 budget is that some people can be tempted to consider “wants” as “needs”.

As with all budgets, this simply means that it requires some self-discipline.

So would you die without having Netflix? Probably not – which means it’s probably not actually a “need”.

Related: The Only Three Budget Categories You Need to Stick to Your Budget

2. Envelope Budgeting

The envelope budgeting method involves allocating a set amount of cash to each budget category for the month.

And once the cash is gone – it’s gone.

(And here’s a tip: our list of the best free budget printables also includes a downloadable template for creating your own budgeting envelopes.)

Who is this for?

This is especially good for people who find themselves overspending when they just rely on credit or debit cards.

Which may sound familiar if you’re the kind of person who swipes first and does the math later.

Instead, actually seeing how much money is left in the relevant envelope can be a great deterrent from spending more than you’d intended.

You can also have as many envelopes as you want, depending on how detailed you wish to be with your budget.

For example, you could have one envelope for utilities.

Alternatively, you could have one for water, one for electricity, one for heating…it’s up to you!

MANAGE YOUR MONEY LIKE A BOSS

Managing your money effectively can literally change your life. And starting a budget using our budget planner is the first step towards you doing just that.

Get it free for a limited time!

You’ll also join our mailing list to get updates on how to manage your money – unsubscribe at any time at the end of each email.

What you should keep in mind

One of the major issues with this budgeting method is the security of it.

Simply put, it’s far safer to carry cards than to carry cash.

And whatever you do, don’t lose the envelopes!

It’s also a short-term fix. That is, if you struggle with money management when using credit or debit cards, this is really something that you need to get under control.

So using the envelope method can be a great way to budget while you rein in your card spending. It may not be a forever fix, though.

Related: The Household Budget Percentages You Should Be Using

3. Zero-based Budgeting

The zero-based budget involves making sure that every dollar has a job.

That is, every cent that comes into your account matches exactly with what’s going out.

This doesn’t mean that you have to spend it all. In fact, some of that money should definitely be allocated to your financial goals, like topping up your emergency fund or your 401(k).

Who is this for?

Fellow control freaks: this one’s for you.

If you’re looking for a way to track all your money and make sure it’s being put to the best use possible (and that, ahem, Saturday night you doesn’t decide to get a bit creative with their money management), the zero-based budgeting method is a great way to do this.

It’s especially good if you’ve had trouble controlling your spending in the past as, this way, you know exactly where it’s all going and can remove any problem areas as soon as they appear.

What you should keep in mind

The pros of this one are also some of its cons.

That is, it can be very detailed and a lot of work.

If you’re committed to this budgeting method, then that’s great!

But if you feel yourself getting a bit tired of tracking every dollar – or know that you won’t be able to sustain it – then this may not be the best option for you in the long term.

It may be best in the case of a zero-based budget to try it for a month, especially if you know you have a particular “black spot” in your money management that you want to work on.

Once you’ve given it a chance, then re-evaluate at the end of the month if it’s working for you – which you could also do for the other budgeting methods too!

Related: The 13 Best Budgeting Apps for Couples

4. Traditional Budgeting

Some things stand the test of time because, simply put, they work.

So the traditional budget may be just what you need for better money management.

Here’s how you do it:

- List all of your expenses then find the total. Just using a pen and paper is fine, or you could even copy and paste these details from your bank statement if most of your spending is done by card.

- Calculate your after-tax income.

- Subtract the first number from the second one.

This is how much you have to play with, whether it be for contributing towards your financial goals or as a bit of extra “fun money”.

However, watch out if the figure is a negative, as it means you’re spending more than you’re earning. Big no-no.

It also gives you the chance to reassess your spending if the resulting figure is less than you’d hoped, like if you wanted to pay off more of your credit card this month.

So once you’ve done this calculation and have the final total, consider where you want to be financially and set some goals.

Having limits on each spending category can really help. For example, you can decide how much you want to spend on necessities like groceries, as well as how much you want to spend on fun things, like a couple of nights out next month.

Also, the list you made at step 1 should really help you to see where you can make some cuts to make sure that you’re actually able to meet those goals.

Who is this the best budgeting technique for?

If you like looking at the nitty-gritty of your finances, this could be the budgeting method you’re looking for.

It’s especially good if you know you’re not doing enough to reach your financial goals – but aren’t sure where to start with reducing your spending.

By having your list of expenditures alongside the final amount of what was leftover at the end of the month, you’ll be able to make adjustments to the spending categories until the final amount is where you want it to be.

Related: 20 Best Books About Budgeting (That You Need to Read)

What you should keep in mind

This one is perfect for those who are detail-oriented.

If you’re not, though, this one could be a struggle.

For example, if your eyes tend to glaze over at a list of numbers, step 1 above could be hell on earth for you.

If that’s you, perhaps take a look at some of the other budgeting methods that use broader categories rather than listing individual expenditures, as one of them could be easier for you to stick to.

5. Continuous budgeting

Continuous budgeting is a budgeting technique often used by companies but could absolutely be used as a personal budgeting method too.

It involves preparing budgets for future periods then revising them on an ongoing basis based on how things are going in the current period.

For example, you would prepare budgets for the first six months of the year. At the end of January, you would look at your progress based on actual spending compared to the goal numbers in your budget.

Depending on how you did, you would then adjust February to June accordingly and create a new budget for July, so you always have six months of budgets ready.

What is the benefit of continuous budgeting?

The main benefit of continuous budgeting is that you’ll always know that you have a short-term (i.e. this month) and a long-term (i.e. the next six months) plan in place.

This is particularly good for knowing what to expect in the coming months. For example, you may have a major expense coming up in March so you can make sure you spend less in January and February to ensure you can cover the March payment.

What you should keep in mind

This takes quite a bit of work to set up at the start as you’ll have to create multiple budgets at once. Some may also find it hard to plan so far in advance.

That said, the future budgets are meant to be updated on an ongoing basis, so you’re not stuck with whatever financial plan you created six months earlier.

But it’s true that if you’re just entering the world of budgeting, this strategy may seem a bit daunting at first.

6. The 60% Solution

This is similar to the 50/20/30 method in that it works using percentages, not set dollar amounts.

It involves you allocating 60% of your income to so-called “committed expenses” which are described as including:

- Basic food and clothing needs

- Essential household expenses

- Insurance premiums

- All of your bills, including non-essentials like Netflix

- All of your taxes

The remaining 40% is divided up into four chunks of 10% as follows:

- Retirement savings: This is where, for example, something like your 401(k) contribution would go.

- Long-term savings: This is money that’s described as being is put into an account that “makes it harder to spend this money without some planning and a series of deliberate steps”. So not your everyday savings or checking account.

- Short-term savings: This money is put somewhere that it can be easily transferred into a checking account, for example, and would be used for things like vacations, repairs and other “irregular but more or less predictable expenses”.

- Fun money: Spend this however you want – but don’t exceed 10%!

Who is this for?

This is perfect for people who are happy to automate a lot of their financial management and don’t wish to track where every single dollar is going.

After all, this strategy lets you assign at least 30% of your expenses to be sent automatically to various accounts that you can’t easily touch.

It’s also one of the best budgeting methods for people who are looking to ramp up their savings. By letting you save 30% of your income (and thus essentially live like you’ve had a 70% pay cut), you’re immediately doing better than the vast majority of people who barely save anything at all.

What you should keep in mind

There are two potential issues with this budgeting method.

Firstly, it’s quite hands off. While this is great for setting-and-forgetting, it can be easy to avoid monitoring this almost at all.

So just make sure you keep at least a small eye on where your money is coming and going so you’re sure you’re sticking to the various percentages.

The bigger possible issue for most people, however, is that you may not be at a point where you can live off what amounts to a 70% pay cut.

Sure, you’re not actually losing 30% of your income – in fact, it’s probably being used the best way possible: to build your financial future!

But changing to a lifestyle where you can survive off that amount probably isn’t going to happen over night, meaning that the 60% solution may have to be something that you work towards rather than immediately implementing.

7. Value-based Budgeting

This is one of the budgeting methods that requires a bit more soul searching than the others.

This is because it involves basing your spending on what you value rather than specific budget categories.

For example, as explained here, you may prefer to not spend much on dining and instead eat at home for a great night in with friends. However, you may also like to travel to see your family who live further away, and so you’re fine with spending more on that type of expense.

This means, when preparing your value-based budget, you’d allocate more money to travel than you would on entertainment costs.

Who is this for?

This is primarily for people who are already good at managing their money and especially those who are very disciplined at controlling their spending or enjoy saving.

If you’re at that stage, you’re probably at the point where you don’t need to track every single dollar. You likely have a good idea already of where your money is going and the fact that your financial journey is heading in the right direction.

This means you may no longer have a need for a super strict budget, although do have some financial goals you’re trying to meet.

In this case, those would become the values that you include when planning where to allocate your money.

What you should keep in mind

This is definitely not for people who don’t already have a good grasp on their finances – and especially those who aren’t good at controlling their spending.

For example, you may like to buy plants, to the extent that your house is starting to resemble a rainforest. If this is you, you could, at this point, consider them as something you value.

But if you really stop and think about it, are plants really, truly something you value – compared to, say, taking a trip once a year to see friends or getting rid of your credit card debt?

One or two plants are fine. A rainforest is probably not.

So if you’re at the rainforest end of the scale, perhaps consider one of the other options on this list.

8. The 80/20 Budget

This one is pretty straightforward: 20% goes to your financial goals before anything else and 80% to the rest.

Some people also refer to this one as the “Pay Yourself First Budget”, perhaps for obvious reasons.

The key here is to make sure you allocate the 20% at the start of your pay cycle, so you’re absolutely sure you have actually paid yourself before everything else.

And then the rest can be used however you want!

Who is this for?

This is one of the best budgeting techniques for those who really want to make sure they’re committing at least some of their income to savings or debt payoff.

It’s also good for not having to keep track of every cent. As long as your spending is within the 80% limit, you can spend that 80% on pretty much anything.

You could also even modify it a bit to be 70/30 or even closer to 50/50, depending on how aggressively you want to – or can – reduce your spending.

What you should keep in mind

This has a similar potential issue to the 60% Solution in that you’ll have to start living like you’ve taken an 80% pay cut.

To be clear, this isn’t necessarily a bad thing! Most of us have areas where we can cut back our spending to focus more on bigger financial goals, so this is a great way to force you to do this.

It can, however, take some adjustment, which is something to take note of when deciding to start this budget.

The other potential issue is that, as mentioned, you won’t be tracking your spending in close detail.

This means that this method may not work for you if you want to reduce your spending in a certain category, like cutting back on grocery costs.

9. The Sub-Savings Accounts Method

You could count this as its own technique, although some may say that it’s a way to implement some of the other budgeting methods.

Firstly, open either multiple savings accounts or, if your bank offers it, multiple sub-accounts within your main savings account.

(Whatever you do, pick an option that doesn’t have any additional monthly fee, even if that means changing banks. You don’t want your reward for good financial habits to be wiped out by bank fees!)

Then name each account or sub-account what the money is being saved up for, such as “Trip to New York” or “New Computer”.

You should then decide on when you want to complete each goal and how much you need for it (e.g. $1,500 for the trip to New York by December, $600 for the new computer by Black Friday).

Finally, divide the amount of money you need by how many months are left until the due date to see how much you need to save each month.

Then set up your accounts so the correct account is automatically deposited in them each time you’re paid. And voila, instant savings!

Who is this for?

This is perfect for people who don’t want to look at specific budget details each month.

Instead, once you’ve set up the automatic transfers, this method is essentially doing the budgeting for you!

Just make sure you’re keeping your spending limit within the amount that you’ve allowed yourself, and you should be good to go.

What you should keep in mind

As with some of the other budgeting methods, the fact that you don’t have to consider each dollar may be a positive for some and a negative for others.

It mainly depends on how disciplined you are. If you think you can manage your spending across the board, then this could be a good one for you.

If, however, you really need to look at how much you’ve spent in each budget category and really see where you cut back on individual ones, you may need more of a hands-on budget technique.

10. Reverse budgeting

For reverse budgets, you focus on achieving one money goal each month. As long as the rest of your money is enough to cover all your other expenses, you can ignore it.

As some examples, your reverse budget could involve:

- Increasing your emergency fund by $500

- Paying $300 off your credit card

- Investing $600 in your 401(k)

And then, once you’ve transferred the money for your monthly goal, all you have to do is make sure you break even on your expenses.

Who is this for?

This is an amazingly simple budgeting method that also makes sure you’re not left wondering why you didn’t achieve some sort of financial goal that month.

This means that you not only save money, but time. No having to review individual expenses each month – just don’t go over the 80% mark and you’re fine.

What you should keep in mind

The simplicity of this budgeting technique can also be its downfall as, like several of the others, it means that you won’t be tracking your spending in individual budget categories.

If you’re trying to control your spending, this one may not be specific enough for you.

That said, anything that gets you saving at least 20% each month definitely has its benefits.

11. The Priority-Based Budget

The priority-based budget forces you to consider just where you really want to be spending your money.

It’s actually commonly used by local governments, but can be a great personal budgeting method too.

You start by listing your different budget categories (including things like paying off debt and contributing to your retirement fund) and then rank them from most to least important.

The idea is that you allocate more money for those things that you consider more important and less for the rest.

Then, when you start to approach your spending limit for the month, you cut back your expenses in the areas that are of a lower priority to you.

Who is this for?

This budgeting technique can work really well for those who feel that budgeting shouldn’t only be a numbers game, but needs to reflect your life too.

This can actually be a great strategy for helping you to stick to your budget. By setting up the priorities based on how you see them, you’ll likely be doing this in a way that best works for your life, even if you don’t mean to.

Ideally, this will make it easier for you to follow when deciding how to use your money throughout the month.

What you should keep in mind

Much like some of the other budgeting methods, there’s a real risk here of you not prioritizing in the best way possible.

If you’re putting “new phone” way higher on the list than “paying off your credit card”, this budget could seriously backfire on your money management plan.

So if you’re considering using the priority-based budget, make sure your priorities are actual priorities that will help your finances.

How many types of budget are there?

There are literally dozens of types of budget out there. Some are, to put it mildly, way more effective than others.

So to save you some time, we’ve whittled down this list to what are easily the 12 best ones.

Of course, what may be the best personal budgeting method for one person might not be so great for you – and that’s ok.

This is why this ultimate guide sets out the pros and cons of each one, so that you can see which type could work best for you.

What is the main purpose of budgeting?

While it may be obvious, the main purpose of budgeting is to make sure you always have a plan on how you’re going to use your money.

That way, you always know that you’ll have enough money for the things you need.

This should include not only your living costs and other similar things, but also the expenses that will make your financial future even stronger than today.

Too many of us live paycheck to paycheck. In fact, one study found that this is true for 78% of US workers.

So by having a budget and making sure that at least some of your money is committed to your financial goals – whether that be paying off debt, contributing to your emergency fund or starting to invest – your actions today are truly going to make you more financially empowered tomorrow.

That means that the answer to the question “what is the main objective of budgeting?” could simply be “to transform your life into what it should be”.

(“Being able to afford an occasional holiday” also works.)

What are the advantages of budgeting?

The advantages of budgeting are almost too many to list, so here are just some examples:

1. Lets you control your money (rather than have it control you)

2. Ensures that you’re always able to contribute to your financial goals

3. Gives you the ability to see any spending problems before they get out of control

4. Allows you to adjust your spending and savings as needed – for example, you may be able to see that you could in fact be contributing more to paying off your debt than you thought

5. Makes sure that you’re prepared for future financial emergencies rather than getting a nasty surprise and not being sure how you’ll pay for it

6. Helps you see whether you could cope with more debt or higher living costs – considering taking on a mortgage or moving to a higher cost-of-living area? If you already have a budget, you’ll easily be able to see if this is feasible for you

7. Provides a great chance for you to discuss money with your significant others – it can be tough to talk about money. So already setting aside some time every month or so, to go through your budget with your significant others to see where adjustments can be made, gives you the opportunity to have those tough but oh-so-important discussions.

8. Reduces stress – money issues are one of the biggest causes of stress so by using a budget, you’re going a long way to helping not only your financial health, but your mental health too

What are the disadvantages of budgeting?

It’s fairly safe to say that the advantages of budgeting far outweigh the disadvantages.

That said, there can be some down sides:

Starting a budget doesn’t immediately mean you’ll stick to it

So you’ve gone through all of these budgeting methods, picked one that works for you and written down all your numbers. Hey, presto! You’re budgeting!

…well, not quite. The most important part of budgeting isn’t actually the budget itself, but the mindset needed to control your spending in a way that helps you stick to what’s in the budget.

Starting a budget can make some people feel like they’ve done all they have to, but it’s only step 1. So make sure you’re in it for the long haul.

It takes time

This is certainly true, especially when you’re just starting out and having to go through all your spending to figure out where you are and when you want to be financially.

But after a month or so, it will become much faster as you get the hang of it. And at the end of the day, wouldn’t you rather spend an hour or so going through your numbers than the rest of your life living with financial stress?

It’s boring

While there certainly may be more fun things to do in life than drawing up a budget, it could be the key to you being able to afford even more fun things, like being able to finally go on your dream holiday.

So spend that not-so-fun hour filling in your numbers – and perhaps include a budget category for a cocktail to reward you for all your hard work afterwards.

(And one way to make it more fun is to use one of the pre-prepared budget planners that are out there. After all, who doesn’t like using sticks to make their budgeting more fun!)

It’s pointless as I’m not wired to stick to a budget

No one is born being better than others at managing their money. In fact, someone who is good at financial management is simply good at consistently maintaining positive money habits.

And much like any habit, it takes time to put in place. So by starting a budget now, it’s true that it may not be easy for you to follow straight away.

But with some practice and time, there’s absolutely no reason why you can’t also learn to put great financial habits in place.

What are some simple budgeting techniques and strategies?

Having some simple budgeting techniques and strategies on hand can be a great way to start on the right foot for sticking to your brand new budget.

Automate your budget as much as possible

Having to actually manage your money yourself takes time, effort and increases the chances of you making a mistake (or, ahem, not doing it at all).

So why bother when you can set up your finances to largely manage themselves!

That is, set up your account so that the day after you receive your income into your everyday account, the amount you’ve allocated for goals is automatically transferred out. Set it up so it’s sent to your savings account, retirement account or wherever else it needs to go to immediately meet your goals for the month.

You can also automate many of your bill payments – bonus points if you call your bill providers and ask them to change your billing cycle so that payment is due right after you receive your income. That way, there’s no chance you won’t be able to pay it off.

Don’t try to achieve everything at once

You’re going to pay off all your credit cards! Contribute to your 401(k)! Make your emergency fund enormous! And that’s only month 1!

Unsurprisingly, this probably won’t stick. So if you have a number of different budgeting goals, pick one to focus on for the next three months. And if you can expand it after that, even better.

By making small changes to your financial habits, it will be way easier for you to actually follow them in the long term.

Make sure you’re really distinguishing between “wants” and “needs”

Many of the budgeting methods in this article involve you allocating a certain amount of money to those things you need and other things you want.

This means that it’s critical to your budgeting success that you don’t put things in the “needs” category that should probably be “wants”.

Similarly, your savings should be a mandatory part of your budget.

You shouldn’t be saving what’s left after a month of eating out and new clothes. Instead, prioritize your needs and financial goals in your budget. Only then should you start to splash out on your “wants”.

So what are the best budgeting methods for you?

The best budgeting methods for you will more than likely not be the same ones for someone else.

It’s going to depend on a variety of things, like how you’re wired. Are you more detail-oriented or do you prefer to look at the bigger picture?

Your current financial situation is also going to play a part. For example, if you’re struggling to make ends meet, it might be a bit much to jump straight into the 80/20 budget.

Essentially, the best personal budgeting methods are those that you’ll stick to. So pick the one that you think will most likely work based on your circumstances to put you on the right track from the start.

READY FOR MORE?

Join thousands of subscribers in getting regular tips in your inbox on how to take control of your finances and save more money – and, for a limited time, get our free budget planner as a gift!

You’ll also join our mailing list to get updates on how to manage your money – unsubscribe at any time at the end of each email.