Having good credit can make a huge difference when you’re considering taking on debt, whether it be for a credit card, a car or a mortgage. But figuring out what is a good credit score range can be tricky.

And it can seem even harder to find out how to get a good credit score.

Fortunately, both are far more straightforward than they first appear.

What is a credit score?

A credit score basically shows a potential lender how much they should trust you.

The higher the number, the more you’ve shown that you’re a trustworthy borrower.

This, in turn, will make lenders more likely to offer you better borrowing terms, such as lower interest rates or a smaller down payment, because you’re seen as being lower risk.

Alternatively, if your credit score isn’t quite as good, you may find that you’re more limited regarding how much you can borrow and what the applicable terms will be.

TAKE BACK CONTROL OF YOUR FINANCES

Our free budget planner will help you to quickly and easily take control of your money – instead of it controlling you.

Get it free for a limited time!

You’ll also join our mailing list to get updates on how to manage your money – unsubscribe at any time at the end of each email.

What is a good credit score range?

Firstly, keep in mind that there are actually different types of credit scores issued by different companies.

However, the two most common ones are the FICO Score, from the Fair Isaac Corporation, and VantageScore, which is jointly developed by the three biggest credit bureaus: Experian, TransUnion and Equifax.

This means that when considering what is a good credit score range, it’s actually worthwhile to look at the numbers in relation to both the FICO Score and the VantageScore, as your potential lender could use either of them.

What is a good FICO Score?

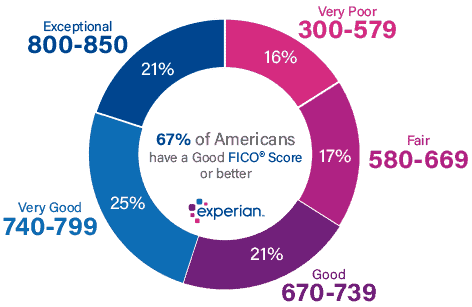

FICO Scores are used in 90% of credit decisions (source) so it’s definitely worthwhile to see where you stand on this front.

While they range from 300 to 850, a FICO Score of 670 and above is considered as being a good FICO Score.

And if you’re wondering about how you’re going compared to the rest of the public, the average FICO Score is 704.

What is a good VantageScore?

While the VantageScore is the most commonly used credit score by lenders after the FICO Score, it’s nowhere near as frequently used.

That said, it can still be helpful to know if you have a good VantageScore or whether it’s something you need to work on.

Like the FICO Score, VantageScores also range from 300 to 850, although lenders look at the numbers slightly differently in terms of assessing whether or not you’re a trustworthy borrower.

In particular, a good VantageScore is considered anything above 700 with the average VantageScore in the US being 675 (source).

Why do I need to have a good credit score?

Having a good credit score can have a major effect on your finances as it’s one of the main things that borrowers look at when deciding whether to lend you money.

Essentially, it’s used by lenders to see how risky you may be as a borrower. If you have a good credit score, you likely have a good credit history which suggests to lenders that you’re likely to repay your obligations.

And the less risky you are, the better your borrowing terms will almost certainly be.

Some of the effects of having a good credit score are listed below.

Personal Capital

Our pick: Best money management app

Easily our choice for the best app to help you manage your money better.

Create a budget, track your spending automatically, receive personalized advice, get alerts about hidden fees and a ton more – and it’s all free.

The interest rates on your loan will be lower, potentially saving you thousands of dollars

Lenders are more likely to offer you a lower interest rate if your credit score is high.

For a major loan like a mortgage, this can end up saving you tens of thousands of dollars over the life of the loan.

Don’t believe me? Check out this calculator to see what a difference this can make.

For example, if you take out a mortgage for a home that costs $400,000 with a 20% down payment of $80,000 for a 30 year term at 4.6%, you’ll pay $270,556 in interest.

But lowering that interest rate by just 1% to 3.6% will involve paying $203,751 over the life of the mortgage.

That is, you’ll save almost $70,000 due to your lower interest rate that you got from your good credit score.

Your insurance may be cheaper

Research has shown that people with bad credit are more likely to file an insurance claim.

It’s for this reason that someone with a good credit score will often pay a lot less for their car and property insurance.

While this isn’t allowed in three US states (California, Hawaii and Massachusetts), the potential benefits in the other states make this a great benefit of having a good credit score.

Related: The Personal Financial Plan Example You Can Use To Reach Your Financial Goals

It can be easier to rent an apartment

Not only does having good credit help you get a mortgage for buying your new home, but it can also help if you’re looking to rent your new place.

Landlords see a good credit score as indicating that you’re more likely to pay rent on time, so will probably consider you more favourably over someone with a worse score.

People with bad credit may also find themselves being charged higher rent to cover the landlord for the risk that you’ll pay your rent payments late – or not at all.

They also (or instead) may have to arrange a guarantor who’ll be responsible for paying for the rent if you fail to do so. This means an extra level of hassle to take care of – when all you want to do is move into your new apartment.

It can be easier to sort out your utilities

Speaking of your new place, utility companies are far more willing to connect you quickly if you have good credit.

However, if you have bad credit, expect to have to pay a deposit or, like with your rent, arrange for a guarantor to get connected.

How is my credit score calculated?

As you’ve seen, figuring out what is a good credit score range isn’t one set answer given that the FICO Score and VantageScore are calculated slightly differently.

That said, overall, they both look at the same factors, even if they give a slightly different weighting to each one.

Seeing as it’s the most common one, we’ll look more closely at the calculation used for the FICO Score (source):

- Payment history (35%): This tells potential lenders whether you’ve consistently made your debt repayments on time. Your score will show how late your payments were, how often you were late, how much you owed and how long it’s been since you last missed a payment.

- Amounts owed (30%): This is based on your credit utilization ratio or what percentage of your available credit you’ve used. The more you’ve used of your total credit limit, the higher your credit utilization ratio will be and the more this can lower your score.

- Length of credit history (15%): By showing that you have a longer credit history in which you’ve consistently made your debt repayments on time, the more you will show potential lenders that you’re a good potential borrower. On the other hand, someone that has only recently taken on credit will be seen as riskier, as there’s nothing to prove how they handle credit.

- New credit (10%): If you open too many accounts or make too many hard inquiries in a short period of time, you’ll appear to be more of a risk and thus your credit score can drop.

- Types of credit used (10%): It’s better for your credit score if you have a variety of credit accounts. This should include both revolving credit lines (e.g. credit cards) and instalment debt (e.g. car loans, student loans).

Now that you know how your credit score is calculated, you can also see where to focus your efforts on improving your credit.

How to get a good credit score?

If you have no or very little credit history, this section will show you how to hit the ground running.

(Keep reading further below for what you can do to improve your credit score if it’s not currently as high as you’d like it to be.)

This is definitely an important part of sorting out your financial future, especially as you’ll likely need to take on some debt in future, even if it’s just getting a credit card.

So starting out on the right track now with your credit can really help you out down the road.

1. Figure out how to manage your money

When used properly, having credit can be great for your finances.

But it can also get people into serious financial trouble, especially if they start using that credit to spend more than they earn or if they take on more debt than they can afford to repay.

In fact, this is often the biggest problem for many people’s financial situation – whether they’re on minimum wage or earning a six-figure salary.

So the first step you should take is to make sure that you become good at managing your money.

Related: How to Drastically Cut Expenses: 43 Easy Ways That Actually Work

The best way to do this is to start a budget so that you know exactly where your money is going in and out.

MANAGE YOUR MONEY LIKE A BOSS

Managing your money effectively can literally change your life. And starting a budget using our budget planner is the first step towards you doing just that.

Get it free for a limited time!

You’ll also join our mailing list to get updates on how to manage your money – unsubscribe at any time at the end of each email.

2. Get a (manageable!) credit card

It’s now time to start building your credit history.

Remember, as mentioned above, you need to show potential lenders that you pay back your debts consistently on time.

Some ways to do this include:

- Sign on to a secured credit card

- Get a store card

- Ask to be added as an authorized user on to someone else’s card

- See if someone will co-sign your card

How to fix a bad credit score?

Figuring out what is a good credit score range is only the first step. The next, most important one, is seeing how to get your own credit score to that point too.

While it’s not an exact science, there are a few things that can definitely help to improve your credit score.

1. Keep an eye on your credit report

According to FICO, the first thing you should do if you’re aiming to improve your credit score is to know exactly what’s in your credit report.

This will let you quickly see if there’s anything that shouldn’t be on there, like mistakes or fraud, which can have a massive effect on bringing your credit score down.

2. Keep your credit utilization ratio below 30% (and, ideally, below 10%)

As mentioned above, your credit utilization ratio is essentially how much you owe divided by your overall credit limit.

It’s based only on your “revolving credit”, which essentially includes credit cards and lines of credit. This means that things like your car loan or mortgage don’t factor into this.

So making sure that your balance on your credit cards is as low as you can make it (and making payments on time by keeping track of your bills!) can be a great way to increase your credit score.

3. Start paying off your debt

This is related to the previous point, but it’s worth repeating: if you’re carrying debt, it’s time to really, truly focus on paying it off.

Not only is it negatively affecting your credit score, but it can also save you a ton of money in interest repayments.

Related: Why Living Stingy Could Be The Key To Achieving All Your Financial Goals

At the same time, you should always make sure that you’re making your debt repayments on time.

If you don’t, not only will you get slammed with late fees, but it can make a mark on your credit report. Not to mention that it may mean you’ll be forced to go through the dreaded process of having to respond to a debt collection letter.

4. Keep old accounts open

Not only can keeping old accounts open be good for your credit utilization ratio, it can also be great for showing the length of your credit history.

And both of these things can really help to improve your credit score.

In fact, the length of your credit history accounts for 15% of your credit score. This means that simply keeping an account open is an easy way to jump a few points.

So when you check your credit report, don’t be tempted to close any old, unused accounts as this can actually hurt your score.

5. Avoid hard inquiries as much as possible

A hard inquiry is what happens when you apply for credit, whether that be a car loan, a mortgage, a student loan or a credit card.

The issue is that when you make one of these credit checks, it shows that a lender has reviewed your credit because you have applied to borrow from them.

This can be a serious problem if you’re trying to work on your credit score, as each hard inquiry can drop your credit score by between five and ten points.

There are two simple ways to avoid this:

- Only make a hard inquiry if you absolutely need to (and only as many times as you need to) OR

- If you need to make multiple hard inquiries, have them done over a short period of time

On the second point, this is because multiple credit inquiries in a two week period (or sometimes 30-day period, but better to be safe than sorry) will only be counted as one inquiry.

So if you’re shopping around for a loan, such as a car loan, a mortgage or a student loan, make it quick and it won’t affect your credit score as much.

Final thoughts

Figuring out what is a good credit score range is only half the battle.

What’s more important is seeing where your score currently is and mapping out a plan to improve it.

With a bit of work and some time, anyone can get there credit score to the “good” range – or even higher!

So take the time to sit down and see exactly how you can work on yours. The potential effect on your finances can be huge.

READY FOR MORE?

Join thousands of subscribers in getting regular tips in your inbox on how to take control of your finances and save more money – and, for a limited time, get our free budget planner as a gift!

You’ll also join our mailing list to get updates on how to manage your money – unsubscribe at any time at the end of each email.